Find the Best Working Capital Loan Now

Interest Rate

9.25%* Per Annual Onwards

Processing Fees

Upto 1% of Loan Amount

Loan Tenure

12 Months

Top Up

Renew Every Year

LTV (Loan to Value)

Upto 150%

You are just a few simple steps away from finding the working capital loan for your business needs. Easy application, quick eligibility check, fast approvals, and get the loan amount on time. From a variety of secured and unsecured working capital loans and direct access to leading lenders from popular banks and NBFCs, the veramigo loan marketplace will always find you a loan to suit your needs. Apply online for Working Capital Loan today.

Picture this: your business is bustling with orders, new clients are lining up, and growth opportunities are knocking at your door. Yet, despite all the excitement, the daily grind—paying suppliers, replenishing inventory, covering utilities, and meeting payroll—feels like running a marathon on an empty tank. This is where working capital swoops in as the unsung hero of your operations. Without it, even the most promising enterprise can stumble, unable to maintain momentum in its day-to-day activities.

Enter the working capital loan—a financial lifeline that ensures your business never runs short on the funds it needs to operate efficiently. Whether you’re facing seasonal dips, planning for an expansion, or simply want to keep operations ticking along smoothly, a working capital loan can inject the liquidity required to keep you ahead of the curve. In this article, we’ll demystify what a working capital loan is, why it matters, and how it can empower you to focus on what truly counts: growing your business with confidence.

What is a Working Capital Loan?

Working Capital Loan is a credit facility offered to startups, business owners, MSMEs and other business entities to manage their daily business operations and enhance business cash flow. It is required for both long-term and short-term financing to meet urgent cash requirements that can be repaid within 12 months. Working Capital Financing offered by banks/NBFCs can be both secured and unsecured loans, as well as in the form of an Overdraft, Letter of Credit and Merchant Cash Advance.

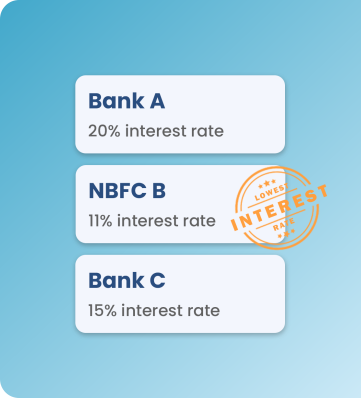

Lowest loan interest rate guarantee

Choose from multiple loan offers and pick the loan with the terms you like most. Based on your Financial Health Card, you will match with banks and NBFCs offering loans to meet your needs. Getting a loan offer? Apply with veramigo and we will match you with a lower interest rate or match the best loan deal.

Fast eligibility check and approvals

Quickly find out your working capital loan eligibility. veramigo checks eligibility criteria from multiple lenders and matches you with lenders who match your criteria. We ensure your business needs are served with quick eligibility checks and fast loan disbursals.

Get flexible loan terms

Connect virtually with lenders from multiple leading banks & NBFCs and choose the right one for you. From working capital needs for MSME to operating capital finance, veramigo lets you negotiate terms you want based on your financial health and needs.

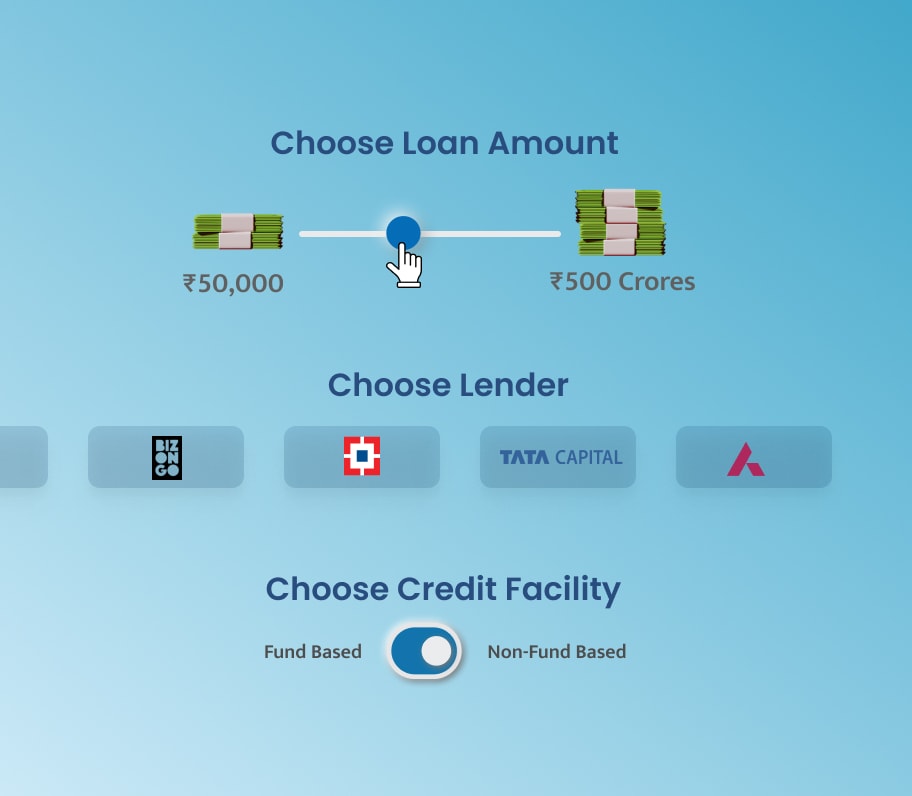

Many secured & unsecured capital options

Getting access to flexible working capital finance like never before. Choose from a range of loans starting from ₹50,000 to ₹500,000,000 offered by a range of lenders on veramigo. Get pre-approved for loans and grow your business with anytime access to various working capital loan options.

Business Loan Process Overview

Identifying Loan's Purpose

Be it for growth, meeting working capital needs, or if you're unsure, we're here to help you figure it out

Business Health Report

Get a quick Business Health Report from veramigo, showcasing your financial health, credit, GST, and banking insights, all consolidated into a snapshot for swift assessment by the Lenders.

Tailored Loan Option

The Loan Marketplace is your key to business success, offering not just loans, but the right loans with terms tailored to your growth ambitions.

Initiate Loan Application

Ensuring you negotiate the terms upfront to avoid any unexpected surprises later.

What Our Customers Say

“It’s a wonderful experience dealing with Veramigo. There staff is will experienced, having complete knowledge of loan procedures. Special thanks to leena Ma’am, she is well trained, experienced and worked very hard on my case. I strongly recommend New Delhi Financial to those who are looking for a loan.”

“Team Veramigo,, Your team is perfect example setter for client service and centricity and also comply norms for FI’s.. Its my previlege to associate with such a team.”

“Veramigo provides the great services with their experienced and staff. They help you with every doubts and suggest what preferred for you, really appreciated.”

Types of Business Loans

There are several working capital loans available in the Indian Financing Market. Some of them are mentioned below:

Overdraft Facility

An overdraft facility allows businesses to withdraw more than the balance in their account up to a certain limit, providing a quick source of funds to cover short-term needs. Interest is charged only on the amount actually utilized, making this option flexible and cost-effective for temporary cash crunches.

Cash Credit (CC)

Similar to an overdraft, a Cash Credit limit is sanctioned against the security of stocks, inventories, or receivables. It enables businesses to borrow funds as needed, maintain liquidity, and ensure smooth day-to-day operations.

Short-Term Business Loans

Traditional short-term loans provide a lump sum amount for a fixed tenure. They come with predetermined interest rates and repayment schedules. While less flexible than an overdraft or credit line, they offer predictable costs and structured financing.

Trade Credit / Supplier Credit

In this arrangement, suppliers grant extended payment terms, allowing a business to procure raw materials or inventory without immediate payment. By aligning payment schedules with revenue inflows, trade credit helps improve working capital cycles without formal interest costs—though discounts for early payment may be forfeited.

Bill Discounting

Under bill discounting, a business can receive early payment on its unpaid invoices at a discount. Instead of waiting for the due date, the company sells its invoices to a financial institution, getting instant funds and improving cash flow. The lender earns a fee, and the business gains immediate liquidity.

Invoice Financing / Invoice Factoring

This is a variation on bill discounting. With invoice factoring, a factor (financial institution) buys your invoices and takes over collections. Unlike discounting, factoring often involves the financier managing the receivables directly, easing the borrower’s operational burden.

Line of Credit (LOC) marginable

A Line of Credit, is a flexible borrowing arrangement between a financial institution and an individual or business. Unlike a traditional loan, where you receive a lump sum, a line of credit allows you to access funds up to a predetermined limit, known as your credit limit.

Types of Interest Rates

Types of interest rates are as follows:

-

Variable Interest Rate

An interest rate that changes based on market conditions. Banks use variable interest rates to protect themselves from market fluctuations, but they can be a bad deal for consumers.

-

Fixed Interest Rate

A common type of interest rate that remains the same throughout the loan term.

-

Compound Interest Rate

An interest rate that’s calculated on both the principal and the interest that’s already been earned. This allows the interest to grow faster.

-

Floating Interest Rate

An interest rate that changes based on market trends. This means that the total interest paid may increase or decrease.

Interest Rates and Repayment

| Types of Working Capital Loans | Min. Interest Rates |

|---|---|

| Overdraft Facility | 9.25% onwards |

| Cash Credit (CC) | 9.25% onwards |

| Short-Term Business Loans | 14% onwards |

| Trade Credit / Supplier Credit | 12% – 16% |

| Bill Discounting | 9% onwards |

| Invoice Financing | 11.30% onwards |

| Line of Credit (LOC) | Marginable depending on the financial institution and other factors. |

Repayment Terms

Working capital loans have a straightforward repayment process. Depending on the lender, you’ll make daily, weekly or monthly fixed repayments. The repayment terms for a working capital loan are typically less than a year, but can range up to 18 months.

Prepayment and Foreclosure

1. Prepayment Charges: For complete prepayment, the fee is generally approximately 4% of the remaining loan balance plus the principal paid in the previous 12 months. Nonetheless, these fees are typically lower than the interest that would accumulate over the remainder of the loan.

2. Foreclosure Charges: Lenders generally determine foreclosure fees as a percentage of the remaining loan balance, typically ranging from 2% to 5%. The fee for complete prepayment is generally greater than for partial prepayment.

Comparison of Business Loan Interest Rates offered by Top Banks/NBFCs

| Bank/ NBFCs | Interest Rate | Tenure | Processing Fee |

|---|---|---|---|

| SBI Bank Business Loan | 14% p.a. onwards | 1-4 years | Up to 2% of loan amount |

| IndusInd Bank Business Loan | 16% p.a. onwards | 1-4 years | Up to 2% of loan amount |

| SMFG Business Loan | 17% – 21% p.a. onwards | 1-4 years | Up to 2% of loan amount |

| Bank of Baroda Business Loan | 17% p.a. onwards | 1-4 years | Up to 2% of loan amount |

| HDFC Business Loan | 14% – 18% p.a. | 1-4 years | Up to 2% of loan amount |

| ICICI Bank Business Loan | 16% – 18% p.a. | 1-4 years | Up to 2% of loan amount |

| Axis Bank Business Loan | 15% – 18% p.a. | 1-4 years | Up to 2% of loan amount |

| Standard Chartered Bank Business Loan | 15% p.a. onwards | 1-4 years | Up to 2% of loan amount |

| Deutsche Bank Business Loan | 16% p.a. onwards | 1-4 years | Up to 2% of loan amount |

| Kotak Mahindra Bank Business Loan | 15% p.a. onwards | 1-4 years | Up to 2% of loan amount |

| RBL Bank Business Loan | 15% p.a. onwards | 1-4 years | Up to 2% of loan amount |

| IDFC First Bank Business Loan | 15% p.a. onwards | 1-4 years | Up to 2% of loan amount |

| Aditya Birla Finance Ltd Business Loan | 17%-18% p.a. onwards | 1-4 years | Up to 2% of loan amount |

| Yes Bank Business Loan | 16% p.a. onwards | 1-4 years | Up to 2% of loan amount |

| Tata Capital Business Loan | 16% p.a. onwards | 1-4 years | Up to 2% of loan amount |

| Hero Fincorp Ltd Business Loan | 16% p.a. onwards | 1-4 years | Up to 2% of loan amount |

| Bajaj Finserv Business Loan | 16% p.a. onwards | 1-4 years | Up to 2% of loan amount |

| NeoGrowth Business Loan | 16% p.a. onwards | 1-4 years | Up to 2% of loan amount |

| U Gro Business Loan | 16% p.a. onwards | 1-4 years | Up to 2% of loan amount |

Working Capital Loan EMI Calculator

EMI Calculator

Loan EMI

Total Interest Payable

Total Payment

(Principal + Interest)

Benefits of Working Capital Loan

- Unsecured loans: When you seek a working capital loan, you don’t need to provide any asset as collateral.

- Swift application and approval procedure: A significant advantage of a working capital loan is the easy application and approval process. Simply provide basic details and submit a few documents to start your application process. The absence of collateral also accelerates the approval process. After your loan receives approval, you can anticipate the allocated amount to be released promptly.

- No interference: Given that this is a temporary loan, you do not need to provide your lender with details about your spending. The lender is not involved in your business affairs, as they have no ownership or share exchange in your company. Your only focus should be on the monthly payments and settling those amounts before the deadline.

- Adaptable withdrawals: Certain companies lack a formal budget or strategy for their finances, particularly regarding the acquisition of new materials or handling overhead expenses. A working capital loan proves useful at this point, providing you the flexibility to utilize funds according to your preference. You do not need to provide an extensive outline of your business’s expenses to obtain the loan. In reality, certain banks provide flexible working capital loans as well. In this case, you only take out what you need and pay interest on that borrowed sum. You can settle your debts whenever you have the funds, without any concerns about prepayment fees.

Eligibility Criteria for Working Capital Loan

Your enterprise needs a consistent cash flow for everyday activities. However, there are occasions when the turnover might fall below your cash flow. If such a scenario occurs, you can always rely on the option of a Working Capital Loan. Before starting the loan application process, it is crucial to review the eligibility criteria for a Working Capital Loan which are mentioned below:

Business Age and Revenue

- Type of Business: The eligibility for working capital loan is determined by the type of business. People, business owners, partnership firms, private or public corporations, retailers, merchants, or any other entrepreneurs involved in service, product manufacturing, or trading sectors that need steady cash flows to sustain their business’s operational capital.

- Business Turnover: The amount of business turnover will fluctuate based on the selected lending bank.

- Business Vintage: A further requirement for qualifying for a Working Capital Loan is the duration of the business. Your business must have been running for the last 2 years while maintaining profitability in your financial statements. Nevertheless, it varies from one bank to another.

- Source of Income: Your business’s source of income is another criterion for eligibility in working capital finance. All revenue for your business is categorized under your income sources, be it from business earnings or investment returns.

How to Apply for a Working Capital Loan

Steps to apply for working capital loan application are as follows:

Documents Required for Working Capital Loan

- Duly filled application form with passport-sized photographs

- KYC Documents of applicant and co-applicants that include Passport, Aadhaar card, Voter ID card, PAN card, Driving License, etc.

- Bank Statement for the past 1 year

- Partnership Deed, if applicable

- Certificate of Company Registration and Incorporation

- Any other document required by the lender

Application Process

-

Step 1

Visit veramigo website to start the process of applying for the loan online. If you are a new user, click on sign up, in case of existing user click on sign in.

-

Step 2

You can register by entering your mobile number and clicking on ‘Next’

-

Step 3

You would receive an OTP, through which you can authenticate your identity.

-

Step 4

Once authenticated with your OTP, you can upload your documents and apply for Working Capital Loan at attractive interest rates as per your requirements.

-

Step 5

Once the loan application form is submitted, the platform connects you with the best lender available as per your requirements. It helps you get a Working Capital Loan at a competitive interest rate.

Approval and Disbursement

After the loan is sanctioned, it usually takes up to four working days for the loan to be disbursed. Lenders often process and disburse working capital loans faster than long-term loans, providing businesses with quick access to funds.

Working Capital Ratios - and its Importance

-

Liquidity

Working Capital Ratios help determine if a business has enough short-term assets to cover its current liabilities. This ensures that the business can meet its short-term obligations and operate smoothly.

-

Operational Efficiency

Proper working capital management can help businesses ensure that they pay their suppliers and employees on time, which can prevent disruptions.

Tips for Choosing the Right Working Capital Loan

It is also necessary to consider aspects such as how often your business has cash flow deficits, the size of the shortfall, the loan’s costs and terms, your qualification requirements, and the flexibility of the financing conditions when sourcing working capital financing.

Here are some tips for choosing the right working capital loan:

1. Compare Interest Rates

When evaluating working capital loans, it’s important to take into account factors such as your credit history, income, and down payment size to assist you in selecting the suitable loan and securing a more favorable interest rate:

- Credit history: A solid credit history may enable you to secure a more favorable interest rate.

- Earnings: A reliable source of earnings can lower the chances of default.

- Down payment: A bigger initial payment can decrease the sum you need to finance and assist you in obtaining improved loan conditions.

- Debt-to-equity ratio: Review your debt-to-equity ratio.

- Loan Duration: Match the loan duration with your business objectives.

Check Loan Terms

- Loan Purpose: Think about why you need the loan, perhaps it is for stock, wages, or vendor payments.

- Loan Amount: Determine the amount of loan needed so you do not borrow too little or too much.

- Payment Schedule: Ensure that the payment schedule aligns with your income cycle.

- Interest rate: Assess their interest rates. Compare how different lenders quote their respective interest rates.

- Additional Costs: Consider the total cost of the loan, involving processing fees, early prepayment penalties, and any hidden fees.

- Credit history: A good credit history would help you get better deal terms.

- Lender’s reputation: Check the reputation of the lender as well.

- Processing time: Choose a lender that facilitates quick approvals and disbursement of funds.

- Sector-specific solutions: Seek lenders that specialize in your industry.

- Collateral requirements: Consider whether you prefer unsecured loans that do not require asset pledging.

Consider Additional Costs

- Compare your cash flow needs and loan term to the business cycle.

- Compare interest rates across lenders, ensuring you understand fixed vs. variable options. Also, check whether there are any hidden charges or not.

- Include fees, such as origination, processing, and prepayment penalties.

- Assess the flexibility of the lender, such as repayment options or early settlement discounts.

- Loan amount must be commensurate to the repayment schedule with the ability to tackle debt management without burdening cash flow.

Common Mistakes to Avoid

Ignoring Credit Score

Your Credit Score is one of the crucial factors of your financial credibility. When applying for a working capital loan, lenders verify this vital aspect to assess your repayment reliability. A poor credit score not only diminishes your chances of securing a loan but also signals potential challenges for future financial endeavours. Keep a regular check on your credit score to enhance your creditworthiness.

Overlooking Additional Costs

There can be certain hidden charges, additional fees or loan expenses that are overlooked while seeking for a working capital loan. Moreover, one often overlooked detail in loan agreements is the provision related to early repayments. While paying off a loan earlier than stipulated might seem beneficial, some lenders impose penalties for the lost interest they would have earned over the loan’s original term. Before finalizing a loan, understand the implications of early repayments.

Not Comparing Loan Options

There are multiple options for working capital loans to be offered, such as lines of credit, short-term loans, and invoice financing. Choosing the wrong type can be expensive. In this digital age, information about lenders and their strategies is more accessible than ever before.

While reviewing interest rates and terms of a loan are part of the decision-making process, researching the reputation of the lenders you are considering should also be considered. Client reviews and ratings, as well as third-party evaluations, may give valuable insights into a lender’s reliability, responsiveness, and overall customer satisfaction.

Working with a trustworthy lender provides more than just favorable rates, but also a hassle-free loan process and better follow-through support. Spending time in conducting proper research will save your business from potential problems and future hassles.

Conclusion

A working capital loan is an essential source of finance for companies that face a need to manage short-term costs and maintain operating efficiency. Understanding the various forms of working capital loans, their features, and their uses will enable firms to make informed decisions that help their financial security and growth. Although working capital loans can provide quick and flexible funding, the associated costs and repayment terms must be reviewed to ensure they meet the company’s financial budget.

Frequently Asked Questions

A Working Capital Loan is a type of short-term financing that businesses use to cover their everyday operational expenses.

Eligibility criteria for a Working Capital Loan are as follows:

- Age criteria: Min. 21 years & Max. 65 years

- Business Vintage: Annual Turnover and Profitability criteria shall be defined by the lender

- Good credit score, financial stability, and repayment history of the applicant

- No previous loan default with any financial institution.

You can submit your application for a working capital loan in two ways. You may access the lender’s official site, download the application form, complete your information, and submit your request. You may also go to the closest branch, ask for an application form, and hand it in along with your documents.

Invoice discounting is the process through which businesses can leverage their receivables to avail financing for any short-term requirements.

Working Capital Loan interest rates start from 9.25%. However, the interest rate can vary depending on the bank or financial institution, as well as the applicant’s business type, revenue and other factors.

A line of credit is a flexible loan that one can access as needed. Interest is charged only on the amount that is utilized and can be repaid either immediately or over time.

The tenure of working capital limit is of 12 months post which the same is reviewed and renewed.

The Working Capital Loan you can avail is determined by Banks and NBFCs. It is based on business profile assessment, financial assessment, past track record, loan amount and tenure.

Working Capital requirement is the difference between Current Assets (namely debtors & inventory ) and Current Liabilities (namely creditors ) of a company. A bank typically funds around 75% of this differential amount. One of the conditions for granting of working capital limits is that the borrower will route all his transactions like sales and purchases, payments of salaries and wages , expenses like electricity, taxes through bank which sanctions the working capital limits.

In order to avail this facility the business concern has to submit stock statements and bills receivable statement every month, based on which the drawing power is set. The term drawing power means the amount of money the bank will allow you to to use, and may vary from month to month depending on the stock position and bills receivable position. In case of services industry such as tour & travel operator , interior firms etc the bank funds a percentage of the receivables or a percentage (typically 20%) of the total receipts. The amount of loan sanctioned depends on the credit policies of the bank and the financial health of the company.

This form of financing is a good source of capital for Small and Medium Enterprises; especially for seasonal or cyclical businesses that don’t have stable sales throughout the year and require liquidity to meet their everyday operating costs. Minimum year of operations of the borrowing company should be 3 years and minimum age group of individuals operating the company should be above 18 years and ideally between 25-30 years .

Working capital limit such as Overdraft can also be applied for by firms in the service industry such as CA, Architects, Interior decorator firms, Lawyers, Tour & Travel operators. They will utilise this credit facility for meeting operating costs such as salaries, office expenses etc.

This credit facility enables business owners to meet their short term obligations. Working capital is crucial for a company’s financial & operational health and helps maintain the profitability of the company. It is basically the difference between the Current Assets and Current Liabilities of a company and helps maintain the working operating cycle and ensures maximization of return on current asset investments.

For example: During peak season, the production capacity of a manufacturing firm is maximised. Working capital requirement is maximum as raw material procurement cost and other operational costs such as wages, transport, packaging etc are high. In case there is a restriction or gap in cash flow of the firm then the entire production process can be slowed down thereby reducing profitability. Hence if the firm has a suitable credit facility to match the cash flows and smoothen the operations, revenue stream will not be adversely impacted and projected profitability can be achieved.

Interest Rate differs of every bank and of every credit facility being availed. The average Interest Rate on a cash credit facility can range from 9% to 13%. The processing fees also varies from bank to bank and can range from 0.75% of the total amount sanctioned to 1.5%.

Interest Rate for unsecured PO funding / Bill discounting ranges from 7.5% up to 18%.